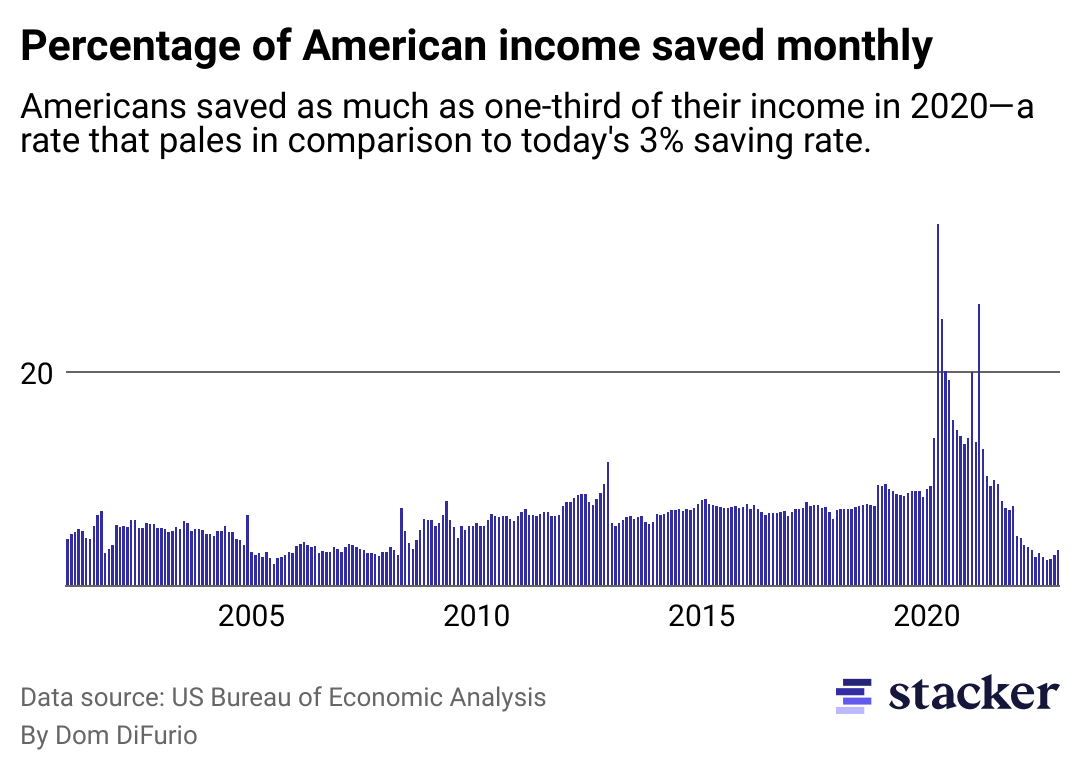

Canva Unusual. Historic. Concerning. These are terms economists use when they look at American saving habits today. Stacker examined what the decline in savings means for the future financial health of the average American. Consumers saved about 3.4% of their monthly income in December, a slight uptick from November’s 2.9%, according to the Bureau of Economic Analysis. That figure has hovered around the lowest since 2005 when the United States was careening toward the Great Recession. At the same time, data suggests Americans have continued spending at rates above pre-pandemic norms. And they’re putting even more expenses on credit cards–a trend that began to pick up in the summer of 2021. The rate is “unusually low,” said Anthony Murphy, a senior economic policy adviser for the Federal Reserve Bank of Dallas. The Personal Saving Rate, a figure economists watch to keep a pulse on the health of consumers from month to month, measures how much income Americans are storing away in a bank account. It is not a measure of the actual amount of money sitting in savings accounts or the equity they may hold in real estate or the stock market. The saving rate provides a sense of how American consumers are behaving at the moment: what decisions Americans are making today as they think about the future and how they’ll cover expenses down the road. As low as the rate is now, it might not be rock bottom, said Olivia S. Mitchell, a professor at the University of Pennsylvania’s Wharton School of Business, where she researches retirement and saving behavior. She said the savings rate could turn negative in 2023, meaning households are spending more than they make in income. ‘The big unknown’

Americans are saving the least they have since 2005. Here’s why that matters.

Feb 15, 2023 | 1:30 PM